Updated May 2026

ITIN Credit Card 2026: Build US Credit Without SSN

5 credit card issuers accept ITIN holders in 2026: Bank of America, Capital One, Deserve, Chime, and OpenSky. You can build a US credit score from zero to 700+ in 12 to 18 months using a secured ITIN credit card. The credit bureaus (Experian, Equifax, TransUnion) create ITIN-linked credit files and score them using the same FICO model applied to SSN holders. A secured card requires a $49 to $500 refundable deposit, reports to all three bureaus, and establishes the credit history you need for auto loans, ITIN mortgages, and premium financial products.

Can You Get a Credit Card with an ITIN in 2026?

Yes. Federal law does not require credit card issuers to use SSNs. The Equal Credit Opportunity Act (15 USC 1691) prohibits discrimination based on national origin in credit decisions. Credit bureaus accept ITINs as valid identifiers and build credit files using the same algorithms applied to SSN-based files.

The key is choosing issuers that explicitly accept ITIN holders. Not every bank does. Applying to the wrong issuer wastes time and creates hard inquiries that lower your score by 5 to 10 points each. Stick to the 5 issuers listed below that have confirmed ITIN acceptance in 2026.

How Credit Bureaus Handle ITIN Credit Files

Experian, Equifax, and TransUnion each create separate credit files for ITIN holders. Your ITIN serves as the unique identifier, just as an SSN does for US citizens. Payment history, credit utilization, account age, and credit mix all factor into your FICO score identically. There is no separate scoring model for ITIN holders.

What Is the Difference Between Secured and Unsecured ITIN Credit Cards?

2 types of credit cards are available to ITIN holders. The right choice depends on your current credit history.

| Feature | Secured Card | Unsecured Card |

|---|---|---|

| Deposit required | Yes ($49 to $500) | No |

| Credit check | Soft pull or none | Hard pull |

| Credit history needed | None | 6 to 12 months |

| Approval rate for ITIN | 90%+ | 50 to 70% |

| Credit limit | Equal to deposit | $500 to $5,000 |

| Best for | Building credit from zero | Existing credit file |

Which Credit Cards Accept ITIN Holders in 2026?

5 issuers have confirmed ITIN acceptance for 2026. Here are the details on each option.

Bank of America Customized Cash Rewards Secured Card

Best overall option for ITIN holders. $0 annual fee, $300 minimum deposit, 3% cashback in a category you choose, and reporting to all 3 bureaus. Requires an ITIN bank account at Bank of America first. Automatic upgrade review after 12 months.

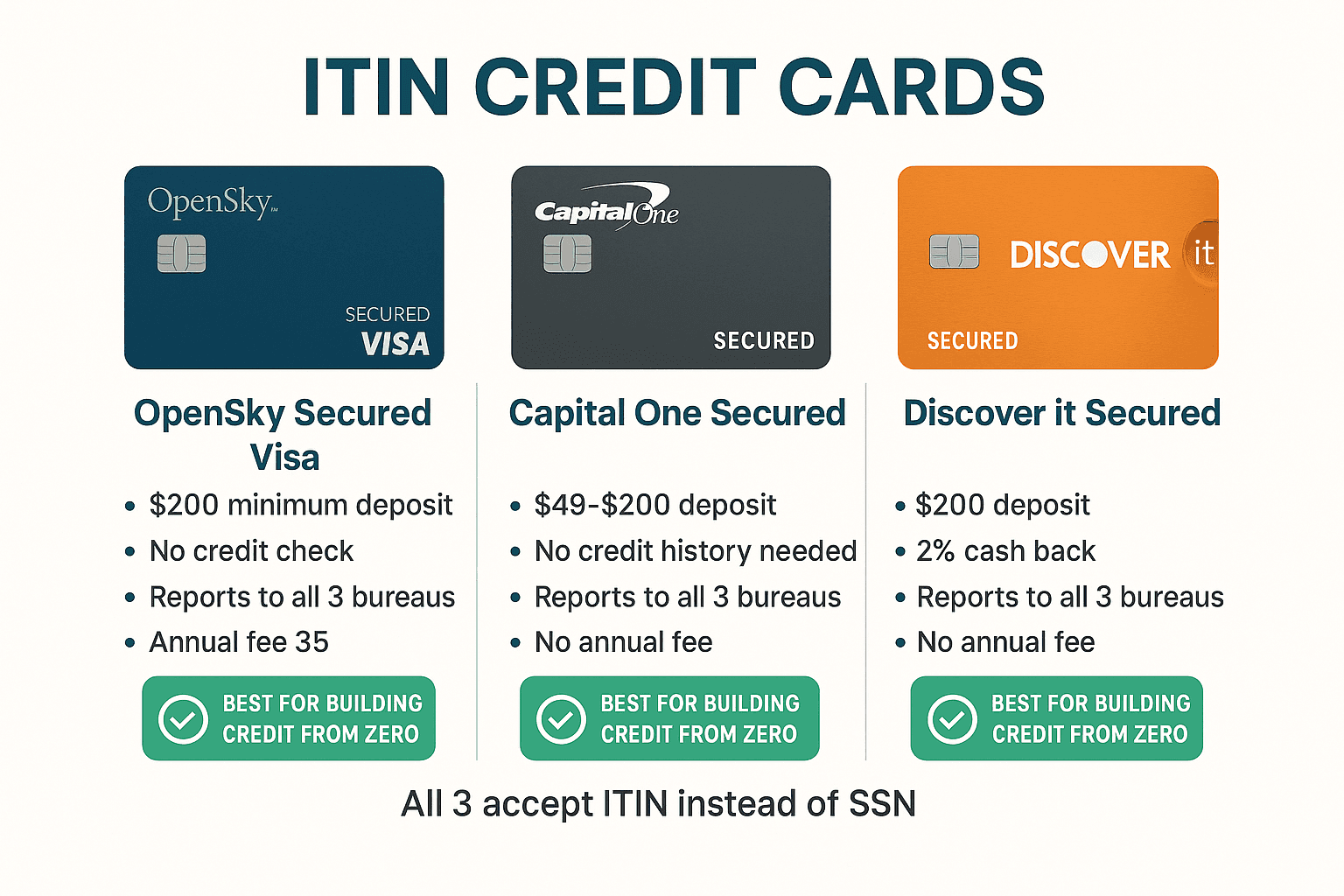

Capital One Platinum Secured Card

Lowest deposit option at $49 to $200 depending on creditworthiness assessment. $0 annual fee. Automatic credit line increase review after 6 months. Capital One accepts ITINs directly on the online application.

Deserve Pro Card

The only unsecured card that accepts ITIN holders with zero US credit history. Deserve uses alternative data (education, international credit) for approval decisions. $0 annual fee, 1% cashback on all purchases, and no deposit required.

Chime Credit Builder Card

No credit check, no annual fee, no interest charges. You load money and spend from your balance. Chime reports to all 3 bureaus. No minimum deposit. Ideal for ITIN holders who want the simplest path to building credit.

OpenSky Secured Visa Card

No credit check and no bank account required. $200 to $3,000 deposit range. $35 annual fee. Reports to all 3 bureaus. OpenSky is a good backup option if you cannot get approved elsewhere.

| Card | Type | Deposit | Annual Fee | Bureaus |

|---|---|---|---|---|

| BofA Cash Rewards | Secured | $300 | $0 | All 3 |

| Capital One Platinum | Secured | $49 to $200 | $0 | All 3 |

| Deserve Pro | Unsecured | $0 | $0 | All 3 |

| Chime Builder | Secured | $0 min | $0 | All 3 |

| OpenSky Visa | Secured | $200+ | $35 | All 3 |

How Do You Build a 700+ Credit Score with an ITIN?

Building a strong credit score requires 5 consistent practices over 12 to 18 months. The FICO scoring model weighs these factors identically for ITIN and SSN holders.

Pay in Full Every Month (35% of FICO Score)

Payment history accounts for 35% of your FICO score. Pay your full statement balance by the due date every month. Set up autopay to prevent missed payments. A single 30-day late payment drops your score by 80 to 110 points.

Keep Utilization Below 30% (30% of FICO Score)

Credit utilization is 30% of your FICO score. If your limit is $500, keep your balance under $150. Below 10% utilization produces the strongest scores. Pay mid-cycle if needed to keep reported balances low.

Keep Your First Card Open (15% of FICO Score)

Length of credit history is 15% of your score. Your first credit card establishes the age of your credit file. Keep it open even after you get better cards. A longer credit history produces higher scores.

Space Applications 6 Months Apart (10% of FICO Score)

New credit inquiries account for 10% of your score. Each hard inquiry reduces your score by 5 to 10 points. Wait at least 6 months between credit applications.

Monitor Your Credit Report (Free)

Check your report at annualcreditreport.com. Under the Fair Credit Reporting Act (15 USC 1681), you are entitled to one free report from each bureau per year. Stagger requests: Experian in January, Equifax in May, TransUnion in September. Report errors within 30 days for fastest correction.

What Is the Timeline to Good Credit with an ITIN?

Here is the month-by-month credit building timeline based on consistent on-time payments and under-30% utilization.

| Timeline | Credit Score | Unlocks |

|---|---|---|

| Month 0 | No score | Secured credit card |

| Month 6 | 580 to 650 | First FICO score generated |

| Month 12 | 650 to 700 | Unsecured card, credit line increase |

| Month 18 | 700 to 730 | Auto loans, apartment rentals |

| Month 24+ | 750+ | Premium cards, mortgage eligibility |

A credit score of 680+ opens the door to ITIN mortgage programs for buying a home. Learn about all the financial products available in our what can you do with an ITIN guide.

What Laws Protect ITIN Credit Card Holders?

3 federal laws protect your rights as an ITIN credit card holder.

Equal Credit Opportunity Act (15 USC 1691)

Prohibits credit discrimination based on national origin, race, or immigration status. Lenders cannot deny your application solely because you have an ITIN instead of an SSN.

Fair Credit Reporting Act (15 USC 1681)

Gives you the right to access your credit report, dispute errors, and receive one free report per bureau per year. These rights apply equally to ITIN holders.

Truth in Lending Act (15 USC 1601)

Requires card issuers to disclose interest rates, fees, and terms clearly before you open an account. Applies to all credit cardholders regardless of tax identification type.

What Are the First Steps to Getting an ITIN Credit Card?

Follow this 4-step process to get your first ITIN credit card.

- Get your ITIN. Apply through itin.so ($297). Processing takes 7 to 11 weeks via IRS Form W-7.

- Open a bank account. Visit our ITIN bank account guide to choose between Mercury, Relay, Wise, or a traditional bank. Bank of America requires an existing account before issuing a credit card.

- Apply for a secured card. Choose from the 5 issuers above. Have your ITIN, passport, and proof of address ready. Deposit $200 to $500.

- Use responsibly for 12+ months. Small purchases, full payments, under 30% utilization. Your score reaches 680+ within 12 to 18 months.

Once you have credit established, explore ITIN real estate investing, freelancing with an ITIN, and PayPal and Stripe verification.

Frequently Asked Questions About ITIN Credit Cards

Need an ITIN to start building US credit? itin.so serves applicants from 150+ countries.

Apply for Your ITIN Today